-

Times of India

| February, 12, 2023Building the supply chain infrastructure for a Circular Apparel industry

Read More -

Livemint

| January, 24, 2023Voluntary carbon trades to start in 2023 -Intellecap report featured in Mint

Read More -

startup20india

| January, 23, 2023Vineet Rai, Founder and Chairman, Aavishkaar Group joins the Sustainability Task Force as part of G20 India Presidency

Read More -

-

hindubusinessline

| December, 23, 2022The SMART AgTech Integration Facility 2022 Bootcamp facilitates over 400 deals between AgTech Startups and Farmers Collectives in Maharashtra at the KISAN Agri Show, Pune

Read More -

PURVANCHAL SURYA

| December, 16, 2022Regional Media Print Coverage of Intellecap and Transform Rural India Foundation’s launch of the Climate Action Platform on 13th Dec with support of Jharkhand State Government

Read More -

Ek Sandesh

| December, 16, 2022Regional Media Print Coverage of Intellecap and Transform Rural India Foundation’s launch of the Climate Action Platform on 13th Dec with support of Jharkhand State Government

Read More -

Dainik Bhaskar

| December, 16, 2022Regional Media Print Coverage of Intellecap and Transform Rural India Foundation’s launch of the Climate Action Platform on 13th Dec with support of Jharkhand State Government

Read More -

News11

| December, 15, 2022TRIF and Intellecap launch Climate Action platform with Jharkhand State Govt. – Extensive Regional Media Coverage

Read More -

Krishijagran

| December, 14, 2022Odisha Govt Launches ‘Odisha AgTech Challenge 2022’: A Joint Endeavour of Govt. of Odisha, World Bank, FCDO and Intellecap – Coverage in Krishi Jagran

Read More - Lack of the implementation of a cohesive milestone-based strategy to decarbonize the supply chain, as well as operations.

- Poor availability of commercially scalable circular, low-carbon technologies that are in sync with the decarbonization needs of the T&A industry.

- Limited awareness and technical capability to measure, report, and set decarbonization goals as per the Science Based Targets

- Emission Mapping & Profiling: Understanding and quantifying carbon emissions across the supply chain, product impact & climate change risks and developing BAU projections.

- Set Roadmap and Create Targets: Developing sustainability strategies, targets and roadmaps at process and organization level, aligned with science and business requirements.

- Reduce Footprint: Identifying & deploying best available technology solutions (input materials, energy efficiency, water mgmt. waste to value, etc) that perform better than the benchmarks; adopting global best practices.

- Adopt offset mechanisms: Address hard-to-abate emissions through off-setting projects such as investing in impact funds, identifying climate finance solutions, etc

- Improvement in energy efficiency: 15 to 20%

- Reduction in process heat: 25%

- Water Recovery: Up to 95%

- Reduction in chemical & biological effluents: 50 to 75%

- Provided end-to-end traceability for ~850 Tons of Textiles waste (2x manufacturers; 4 months)

- Solutions indicated a payback period of 2 to 3 years

(work to measure the impact on carbon footprint is currently in process) - The ability of CAIF to source and evaluate high-potential innovative solutions

- Technical assistance provided by CAIF to innovators (from problem-solution through product-market fit) and the capacity building support provided to manufacturers and supply chain partners

- Provision for a pool of capital available for both innovators and brands /manufacturers to cover the cost of demonstration pilots that expedited approvals & enabled collaborations

Building the supply chain infrastructure for a Circular Apparel industry

Mumbai, 13th February –Siddharth Lulla, Principal, Circular Apparel Innovation Factory (CAIF), Intellecap was recently featured on the Times of India blogs through his article, “Building the supply chain infrastructure for a Circular Apparel industry” which highlights how CAIF is working with upstream supply chain partners primarily SMEs to reduce carbon emissions,

Under the aegis of UN Climate Change, brands and retailers worked during 2018 to identify ways in which the broader textile, clothing and fashion industry can move towards a holistic commitment to climate action. As a result, industry players made bold commitments to enable circularity, reduce 45% emissions by 2030 and achieve net-zero by 2050. Initially these commitments were focused on Scope 1 and Scope 2 emissions, which are produced by the companies directly or through the purchase of energy. However today, most companies have pledged to reduce their Scope 3 emissions generated in the upstream and downstream value chain. This is a crucial step since, for many companies, Scope 3 accounts for 80% of their overall climate impact.

Given the scale of the problem, it is imperative to set ambitious targets and implement a well thought approach to deliver on them. Achieving net-zero for Scope 1 and Scope 2 themselves requires overcoming formidable economic and technical challenges. Scope 3 presents an additional layer of complexity such as aligning internal stakeholders on goals and milestones; working collaboratively with supply chain partners, customers; keeping all partners engaged in multiyear change efforts; non-transparent carbon accounting and tracking mechanisms.

An in-depth assessment through in-person consultations with Textile & Apparel (T&A) stakeholders, which included industry leaders such as H&M, IKEA, Marks and Spencer and their manufacturing partners, and learning’s from our initiatives have identified key gaps that need to be addressed to develop the supply chain infrastructure for circular and net-zero apparel:

Hence Intellecap, through its initiative Circular Apparel Innovation Factory (CAIF), is working with upstream supply chain partners primarily SMEs to reduce carbon emissions, through testing, validating and commercial adoption of circular and low-carbon solutions in resource efficiency (energy, water), alternate materials (low-carbon dyeing alternatives, etc.), and from recovering value from waste (fiber2fiber recycling). Based on our learnings, we believe that four steps need to be followed by organizations that are committed to multiplying their own efforts and decarbonizing the supply chain through supplier engagement. They are:

Research findings have indicated that existing solutions which include renewable electricity, sustainable materials and processes, alternate fuels, etc., have the potential to reduce supply chain carbon emissions by 47%. However, for the balance there is a need to test, validate and adopt innovative technologies and business models such as next generation materials, waterless dyeing, dry processing just to name a few. In order to address this, through our ongoing initiatives we have successfully worked towards building a strong business case for low carbon / circular supply chain solutions available in India. Project ACE, a two-year program (2021-2023), designed as a common action platform with the singular purpose of establishing a business case (economic value creation for the private sector organizations while reducing their environmental footprint). To create a robust business case, CAIF designed demonstration pilots with multiple stakeholders (brands and their manufacturing partners) to test, validate and commercially deploy high potential low-carbon solutions in areas including energy efficiency, water efficiency, alternative dyes and chemicals, digital solutions in textiles waste traceability, etc.

In the last 12 months alone, we have undertaken six pilots and delivered the below outcomes:

According to our private sector partners, three key aspects were critical in design /execution of the pilots along with expediting the buy-in from leadership / board teams for eventual long-term commercial contracts:

Hence based on these learnings we believe there is a need for and are working towards designing long term transformation programs with brands and their supplier networks to lay the foundation of a circular supply chain infrastructure and catalyze their journey to NetZero.

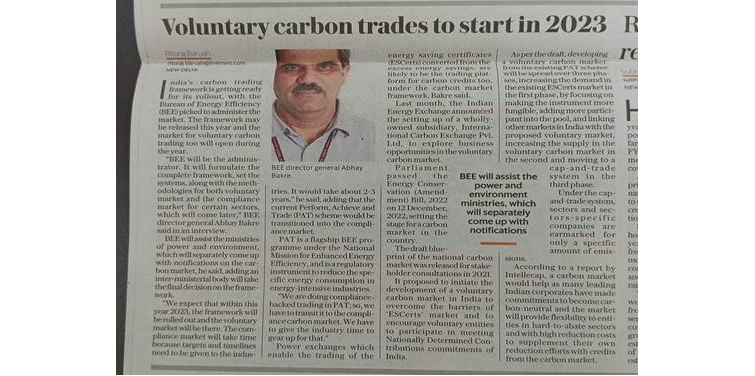

Voluntary carbon trades to start in 2023 -Intellecap report featured in Mint

Mumbai 24th Jan– Mint’s story (Print and Online) titled ‘Voluntary Carbon trades to start in 2023’ featured the Intellecap report on carbon markets and highlighted the India’s carbon trading framework with details from Bureau of Energy Efficiency (BEE) with whom the Intellecap Climate team works extensively.

India’s carbon trading framework is getting ready for its rollout, with the Bureau of Energy Efficiency (BEE) picked to administer the market. The framework may be released this year and the market for voluntary carbon trading too will open during the year.

“BEE will be the administrator. It will formulate the complete framework, set the systems, along with the methodologies for both voluntary market and the compliance market for certain sectors, which will come later,” BEE director general Abhay Bakre said in an interview.

BEE will assist the ministries of power and environment, which will separately come up with notifications on the carbon market, he said, adding an inter-ministerial body will take the final decision on the framework.

“We expect that within this year 2023, the framework will be rolled out and the voluntary market will be there. The compliance market will take time because targets and timelines need to be given to the industries. It would take about 2-3 years,” he said, adding that the current Perform, Achieve and Trade (PAT) scheme would be transitioned into the compliance market.

PAT is a flagship BEE programme under the National Mission for Enhanced Energy Efficiency, and is a regulatory instrument to reduce the specific energy consumption in energy-intensive industries.

“We are doing compliance-backed trading in PAT; so, we have to transit it to the compliance carbon market. We have to give the industry time to gear up for that.”

Power exchanges which enable the trading of the energy saving certificates (ESCerts) converted from the excess energy savings, are likely to be the trading platform for carbon credits too, under the carbon market framework, Bakre said.

Last month, the Indian Energy Exchange announced the setting up of a wholly-owned subsidiary, International Carbon Exchange Pvt. Ltd, to explore business opportunities in the voluntary carbon market.

Parliament passed the Energy Conservation (Amendment) Bill, 2022 on 12 December 2022, setting the stage for a carbon market in the country.

The draft blueprint of the national carbon market was released for stakeholder consultations in 2021. It proposed to initiate the development of a voluntary carbon market in India to overcome the barriers of ‘ESCerts’ market and to encourage voluntary entities to participate in meeting Nationally Determined Contributions commitments of India.

As per the draft, developing a voluntary carbon market from the existing PAT scheme will be spread over three phases, increasing the demand in the existing ESCerts market in the first phase, by focusing on making the instrument more fungible, adding more participant into the pool, and linking other markets in India with the proposed voluntary market, increasing the supply in the voluntary carbon market in the second and moving to a cap-and-trade system in the third phase. Under the cap-and-trade system, sectors and sectors-specific companies are earmarked for only a specific amount of emissions.

According to a report by Intellecap, a carbon market would help as many leading Indian corporates have made commitments to become carbon-neutral and the market will provide flexibility to entities in hard-to-abate sectors and with high reduction costs to supplement their own reduction efforts with credits from the carbon market.

The market would incentivize entities with low reduction costs to reduce emissions beyond their mandate. Trading in the carbon market could reduce the overall cost of emission reductions in India, it said.

Vineet Rai, Founder and Chairman, Aavishkaar Group joins the Sustainability Task Force as part of G20 India Presidency

Mumbai, 23rd Jan: Vineet Rai, Founder and Chairman, Aavishkaar Group has joined the sustainability task force as part of the new engagement group StartUp20, initiated under India’s presidency of G20.

The Inception Meeting for #Startup20 marks the beginning of an incredible journey to foster innovation and growth in the global startup ecosystem. At this historic event, we will be introducing the 3 task forces that will drive the vision and mission of Startup20 India

One of the key ways that startups promote a nation’s growth and economic stability is through the aspect of employment creation. Startup20 is a significant step in the direction of encouraging innovation and entrepreneurship on a global scale, which will ultimately result in more job opportunities.

Startup20 Inception Meeting – Hyderabad

Date – 28 – 29 January 2023

To know more – Click Here

How to make a Purpose Driven Startup Ecosystem a Reality

Mumbai, 10th Jan: Listen to the two part special podcast on “How to make a Purpose Driven Startup Ecosystem a Reality” as part of Aawaz.com and Reverie Language Technologies “ Building for Bharat”Season 2.

The two part podcast features Vineet Rai, Founder and Chairman, Aavishkaar Group and Nayan Kalnad, Founder and CEO, Avegen, and host , Arvind Pani, CEO and Co-Founder, Reverie Language Technologies, and highlights the critical factors which will play an integral role in making a thriving startup ecosystem and realizing the dream of an Atmanirbhar Bharat.

In the first podcast, Vineet, Nayan and Arvind discuss the fascinating evolution of the Bharat startup ecosystem and its key challenges, the rising aspirations of a digitally empowered Bharat and delves deep into the potency of digital adoption.

Building for Bharat / Season 2 / To listen to Part 1 – Click Here

In the second podcast, the speakers dispel some myths around the Bharat consumer, dissects the anatomy of a robust and dynamic Bhaart business and discusses the role of entrepreneurs in leveraging the advances in digital to come up with solutions which make a difference, and delivers maximum impact.

Building for Bharat / Season 2 / To listen to Part 2 – Click Here

The SMART AgTech Integration Facility 2022 Bootcamp facilitates over 400 deals between AgTech Startups and Farmers Collectives in Maharashtra at the KISAN Agri Show, Pune

Mumbai 23rd Dec– The SMART AgTech Integration Facility (SAIF), a collaboration between the Government of Maharashtra and the World Bank Group, held a Bootcamp at the KISAN Agri Show in Pune from December 14-18, 2022. The event featured over 35 Disruptive Agriculture Technology (DAT) companies and was attended by more than 200 farmer collectives (CBOs). As a result of the Bootcamp, over 400 agreements were made to introduce digital and technical solutions to the CBOs throughout Maharashtra.

Over 35 Disruptive Agricultural Technologies (DAT) solution providers across India showcased their products to more than 200 farmer collectives (CBOs) at this initiative by Government of Maharashtra and World Bank.

The SMART Agtech Integration Facility 2022, powered by Intellecap, is a project led by the Hon. Balasaheb Thackeray Agribusiness and Rural Transformation (SMART) initiative in rural Maharashtra. The project, which is supported by the World Bank Group and the Korea-World Bank Partnership Fund (KWPF), is focused on supporting the development of inclusive and competitive agriculture value chains and helping smallholder farmers, collectives, and agri-entrepreneurs in Maharashtra. The Complimentary Innovation Investments (CII) sub-component of the SMART project is formulated to promote the adoption of agricultural technology solutions among selected farmer organizations in the state.

The event was organized under the leadership of Hon. Kaustubh Diwegaokar, Project Director of the SMART project, Shri. Dyaneshwar Bote, APD, Shri. Vijay Kolekar, Capacity Building Expert, and Dr. Preeti Sawairam, Technical Officer – Complimentary Innovation Investments (CII) from the SMART project.

During the event, Hon. Kaustubh Diwegaokar, Project Director, SMART emphasized that “the SMART project is committed to establish the SMART AgTech Integration Facility to help farmers and their collectives in Maharashtra access innovative technologies. The Bootcamp is an important step in building partnerships between DAT solution providers and Community-Based Organizations (CBOs) to enable farmers to access more lucrative markets and achieve greater economic returns.”

Rahul Agrawal, Director, Intellecap, commented on the SMART Agtech Integration Facility, stating that “Intellecap is facilitating the SMART project in the operationalization of the facility and has analyzed more than 100 AgTech enterprises for participation in the initiative. This facility is expected to benefit more than 40,000 farmers in Maharashtra. The project aims to assist farmers and their collectives in digitizing the farming operations, improving farming systems through precision farming, leveraging urban markets through improved logistics and linkages, and increasing access to finance. SMART plans to expand the usage of DAT solutions by CBOs across the state and the deals made here will serve as a model for developing a supportive ecosystem”

The KISAN Agri Show is India’s largest agriculture expo, running for more than 29 years, which brings together agri-professionals, policymakers, government officials, media, and like-minded individuals from across India to discuss the future of the Indian agriculture sector and is attended by over 100,000 farmers.

Dr. Dinesh Chauhan, VP, new initiatives at DeHaat, one of the 35 DAT enterprises featured at the Bootcamp, shared that “DeHaat is eagerly looking forward to work with the CBOs under SMART program and the response we received from various CBOs during the recently concluded bootcamp at KISAN 2022 in Pune is very encouraging. We will be extending our digital solutions to CBOs through our various digital applications like Farmer App, Extension App, Business App and will be offering localized crop solutions along with critical agri inputs to these CBOs along with financial products. We will be looking forward from the program to support these CBOs to avail these digital solutions and enable them to become self-sustainable. We will also be connecting these CBOS through our platform to market as well, which will eventually lead to better realization of farm produce.”

Saurabh Sharma, Lead Institutional Business at FASAL added that “through the SMART initiative, FASAL was able to reach a large number of farmers and CBOs. We plan to help these CBOs and its members increase their productivity, quality, and reduce their input costs and losses from various infestations. We are excited to see the interest of the CBOs in our enterprise and the opportunity to meet so many farmers and their collectives under one roof was very advantageous.“

Regional Media Print Coverage of Intellecap and Transform Rural India Foundation’s launch of the Climate Action Platform on 13th Dec with support of Jharkhand State Government

Regional Media Print Coverage of Intellecap and Transform Rural India Foundation’s launch of the Climate Action Platform on 13th Dec with support of Jharkhand State Government

Regional Media Print Coverage of Intellecap and Transform Rural India Foundation’s launch of the Climate Action Platform on 13th Dec with support of Jharkhand State Government

TRIF and Intellecap launch Climate Action platform with Jharkhand State Govt. – Extensive Regional Media Coverage

Mumbai 15th Dec– Transform Rural India Foundation and Intellecap launch Climate Action platform with support of Jharkhand State Government to enable smallholder farmers– Follow the Regional Coverage

Platform will enable smallholder farmers with additional resources and knowledge to undertake climate change mitigation and adaptation activities by leveraging climate and carbon finance

Intellecap and Transform Rural India Foundation (TRIF) announced the launch of a Climate Action Platform with the support of the Jharkhand State Government on the 13th of Dec at Hotel Chanakya, BNR Ranchi.

The platform, launched by Anish Kumar, MD, TRIF and Santosh Kr. Singh, MD – Agri and Climate, Intellecap, will enable smallholder farmers from the state to leverage climate/carbon finance for agriculture and allied sectors and develop their technical skills through a capacity-building program. The platform will provide support and training to smallholder farmers for climate smart agriculture and agro-forestry.

The Climate Action platform was launched during an exclusive workshop, where keynote addresses were made by Senior State Govt. officials, Senior Leaders from Intellecap and TRIF, and attended by the farmer organizations, academic and research organizations, NGOs, Agtechs, financiers, to create awareness about climate-resilient agriculture and the role to be played by the Intellecap-TRIF platform.

Smt. B Rajeshwari, IAS, MGNREGA Commissioner, Rural Development Dept., Dr. Shivendra Kumar, Former President, ICAR RCER, Eastern Zone, Jitendra Kumar Singh, IAS, Industry Dept., Sanjeev Kumar, IFS, Sashi Ranjan, IAS, Deputy Commissioner, Khunti Jharkhand and Koyel Mandal, Chief of Programs, Shakti Sustainable Energy Foundation spoke at the event which also had a panel discussion on the impact of climate change on the smallholder farmers of the state and key interventions to undertake climate change adaptation and mitigation in the agri and forestry sector.

The Group was well represented through Santosh Kr Singh, MD, Intellecap who launched the platform and by Sanchayan Chakraborty, Partner, Aavishkaar Capital who spoke about the importance of Climate Finance.

In the pic- Attendees to the workshop with TRIF, Intellecap leaders and State Govt. Dignitaries

Coverage in News 11

Regional Media Coverage (In Print)

The launch was covered by all the regional dailies namely Dainik Bhaskar, Jharkhand Darshan, Purvanchal Surya, Bihan Bharat, Ek Sandesh, Punch, Jharkhand Ujwala, Naveen Mail, Prabhat Khabar, Rashtriya Khabar, Deshpran to name a few

Odisha Govt Launches ‘Odisha AgTech Challenge 2022’: A Joint Endeavour of Govt. of Odisha, World Bank, FCDO and Intellecap – Coverage in Krishi Jagran

Mumbai 14th Dec– The Government of Odisha, with funding from the World Bank and the Foreign, Commonwealth & Development Office of UK, has launched the ‘Odisha AgTech Challenge 2022’ at the 3rd Make in Odisha Conclave 2022. The Challenge was enabled by Intellecap.

The agricultural sector in Odisha engages ~60% of the total workforce and accounts for ~18% of Gross State Domestic Product (GSDP). While there has been a positive trend in farmers’ income in the state, this is a pivotal opportunity to leverage technology to bolster this trend further.

The challenge aims to solve critical issues in key agriculture value chains and increase farmer profitability in Odisha. The challenge was launched under the guidance of Pradeep Kumar Jena, IAS, Agriculture Production Commissioner -cum- Additional Chief Secretary, Arabinda K Padhee, Principal Secretary, DA&FE, Asit Tripathy, IAS (Retd.), Principal Advisor to Chief Minister, Prem Chandra Chaudhary, IAS, Director of Agriculture & Food Production, Sanjeev Kumar Chadha, IFS, Special Secretary, Dept. of Agriculture & Farmers Empowerment, and Rohit Kumar Lenka, IFS, Director of Horticulture, Govt of Odisha. GDi Partners and Intellecap, a global impact advisory firm, is supporting the execution of the challenge.

This Challenge is presently seeking applications from AgTech Enterprises that are working in key agriculture value chains to test or scale their product through a pilot project in the state, as well as providing farmers with access to affordable, modern-age solutions to the challenges they face. Selected AgTech Enterprises will receive financial support through grants to scale-up their operations, as well as outreach, incubation and mentorship support, and on-ground network support to conduct pilots in Odisha.

The Odisha AgTech Challenge is part of the ‘Modernizing Agriculture and Allied Sector’ or MAAS-O programme, where GDi Partners along with the World Bank are leading the creation of a strategy for the State Government to align with the “One Nation, One Market” initiative of the Union Government, for enhancing state capacity, improving coordination among the various departments working for farmers’ welfare and leveraging innovative agriculture technologies to fast-track an increase in farmers’ income.

Speaking at the launch, Arabinda K Padhee, Principal Secretary, DA&FE said, “The Government of Odisha is committed to catalyzing an increase in farmer incomes across the state by partnering with the private sector in Odisha to improve the efficiency of agricultural supply chains, financing facilities and marketing. We are excited to launch the Odisha AgTech Challenge 2022 to promote innovation & technology while improving state-wide agricultural productivity and efficiency”.

The agricultural sector in Odisha engages ~60% of the total workforce and accounts for ~18% of Gross State Domestic Product (GSDP). While there has been a positive trend in farmers’ income in the state, this is a pivotal opportunity to leverage technology to bolster this trend further. The Challenge, led by the Department of Agriculture and Farmers’ Empowerment (DA&FE), has partnered with the Department of Fisheries and Animal Resources Development (F&ARD), the Odisha Millets Mission and Startup Odisha to further this initiative.

Dr. Oliver Braedt, Practice Manager, Agriculture and Food Global Practice (South Asia) for the World Bank, said, “The Odisha AgTech Challenge addresses a critical challenge of harnessing the innovation and dynamism happening in the digital agriculture space to improve outcomes for farmers in Odisha through supporting selected Enterprises to conduct pilot projects. This Challenge has the potential to demonstrate innovative solutions that can be scaled up across the country.”

The Odisha AgTech Challenge 2022 is seeking applications across 6 themes: Market Linkage Solutions, Satellite-based Services, Crop Advisory, Access to Agriculture Inputs and Fodder, Access to Finance, and Post-Harvest Processing and Storage. AgTech Enterprises with a specific focus on agriculture, especially millets, fisheries, animal husbandry, and horticulture, are welcome to apply.

According to Pravanjan Mohapatra, AVP at Intellecap, “The Odisha AgTech Challenge is a novel way for AgTech Enterprises to test and validate their minimum viable product in a supportive ecosystem, the underlying impact and knowledge of which will be very significant for the agriculture sector in Odisha as well as for the whole country. We are excited to work with the Govt. of Odisha, the World Bank and other key partners in finding Enterprises who will be joining us in this journey to help transform Odisha through their innovative solutions, which in turn will enable farmers, address critical challenges across the value chain, and improve agricultural productivity”.

Our Impact Map